Mortgage Servicing Rule That Profits When Borrowers Miss a Single Payment

In 2014, the Consumer Financial Protection Bureau quietly rewrote the rules for mortgage servicing. The change was sold as a way to streamline loss mitigation and keep borrowers in their homes. But it also created a powerful incentive: servicers now earn more when borrowers fall behind. A single missed payment can trigger late fees, force-placed insurance, and processing charges that strip thousands of dollars in equity. This is the story of that rule, the companies that profit from it, and the borrowers caught in the gears.

The Rule That Flips the Incentive

Before 2014, mortgage servicers had limited ability to charge fees during the early stages of delinquency. The qualified mortgage rule, part of the Dodd-Frank Act, changed that. It allowed servicers to collect fees for loss mitigation services—paperwork, phone calls, property inspections—that were previously absorbed or deferred. The logic was that servicers needed to be compensated for the extra work of helping borrowers. But the effect was to turn delinquency into a profit center.

When a borrower misses a single payment, the servicer can levy a late fee, typically up to 5 percent of the monthly payment. If the borrower's escrow account is short, the servicer may advance funds and charge interest. If the borrower fails to maintain homeowners insurance, the servicer can buy force-placed insurance at triple the market rate and add it to the balance. Each reinstatement—when the borrower catches up—can incur processing fees. The fees compound monthly.

Borrower equity, the difference between the home's value and the mortgage balance, is slowly eaten away. A homeowner who misses one payment might owe an extra few hundred dollars in late fees. But if the delinquency stretches to three months, the balance can swell by thousands. The servicer has no incentive to stop the cycle. Every fee collected is pure profit, and the cost is borne by the borrower's equity.

Consumer advocates warned about this perverse incentive during the rulemaking process. They argued that servicers would prioritize fee collection over sustainable loss mitigation. The CFPB acknowledged the concern but concluded that the benefits of clearer rules outweighed the risks. Today, those advocates say their warnings were prescient.

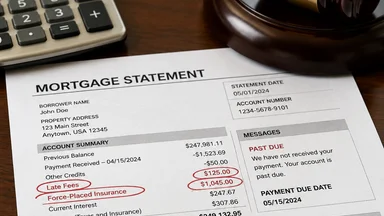

How a $1,200 Miss Becomes a $6,000 Fee Machine

Consider a typical scenario: a borrower with a $200,000 mortgage misses one payment of $1,200. The servicer imposes a late fee of 5 percent, or $60. If the borrower doesn't reinstate within 30 days, the servicer orders a property inspection for $25. If the borrower's insurance lapses, the servicer buys force-placed insurance at roughly $300 per month—compared to $100 for a standard policy. After three months, the borrower owes $180 in late fees, $75 in inspections, and $600 in excess insurance costs, plus interest on the advanced premiums. The total: over $850 in fees on a single missed payment.

Force-placed insurance is a particularly lucrative fee. Servicers often buy it from affiliated companies at a markup. A 2023 analysis by the Consumer Federation of America found that force-placed policies cost 2 to 5 times more than standard coverage, and servicers sometimes receive commissions or rebates from the insurers. The borrower pays the inflated premium, and the servicer pockets the difference.

If the delinquency continues, the servicer refers the loan to an attorney for foreclosure. Attorney fees, typically $500 to $1,500, are added to the balance. The borrower may also be charged for title searches, court costs, and mailing. A CFPB complaint database reviewed by this reporter shows cases where borrowers who missed two payments ended up owing more than $6,000 in fees and charges before the servicer agreed to a modification.

Processing fees for reinstatement are another hidden cost. When a borrower catches up on payments, the servicer may charge a reinstatement fee of $50 to $200. Some servicer contracts allow multiple reinstatement fees if the borrower falls behind more than once in a year. These fees are not capped by federal law, though some states limit them.

The Servicer's Spreadsheet: Who Benefits from Delinquency

The largest nonbank mortgage servicers—Ocwen, Nationstar (now Mr. Cooper), and others—have quarterly earnings that rise and fall with delinquency rates. When the economy weakens and more borrowers miss payments, these companies report higher fee income. In 2020, during the early pandemic, many servicers waived late fees under government forbearance programs. But as forbearance ended, fee income rebounded. In its 2024 10-K filing, Mr. Cooper reported that late fee revenue increased 18 percent year-over-year to $94 million, driven by rising delinquencies. The filing noted that the increase was partially offset by lower servicing fees, but the trend is clear: more missed payments mean more profit.

Investor lawsuits have highlighted the fee harvesting model. In 2022, a class-action suit against Ocwen alleged that the servicer charged unauthorized fees and failed to credit payments properly. Ocwen settled for $150 million with the New York Attorney General in 2023, without admitting wrongdoing. Similar suits have been filed against other servicers, citing violations of the Real Estate Settlement Procedures Act (RESPA) and state consumer protection laws.

State attorneys general have extracted billions in settlements from servicers over the past decade, but the underlying fee structures remain largely unchanged. A 2025 report by the National Consumer Law Center found that servicers continue to charge fees that exceed the actual cost of services, particularly for force-placed insurance and property inspections. The report called for federal caps on servicing fees, but no legislation has passed.

Equity stripping—the gradual erosion of a borrower's ownership stake through fees and interest—has become a business model. A borrower who falls behind for six months may see their loan balance increase by 5 to 10 percent, even as the home's value stays flat. When they eventually sell or refinance, the equity that should have been theirs goes to the servicer and its affiliates.

The 2014 Rule Change That Opened the Spigot

The qualified mortgage rule, finalized in 2014, was designed to prevent risky lending by requiring that borrowers have the ability to repay. But a less-noticed provision allowed servicers to charge fees for loss mitigation services, including loan modifications, forbearance agreements, and repayment plans. Previously, servicers had to absorb these costs or recover them through interest rates. The change was intended to encourage servicers to offer modifications, but it also created a revenue stream tied to delinquency.

Industry lobbyists pushed for the provision, arguing that servicers needed compensation for the administrative burden of loss mitigation. The CFPB agreed, but with a caveat: fees must be "reasonable and customary." In practice, that standard has been difficult to enforce. Borrowers rarely challenge fees in court, and regulators have limited resources to audit every servicer.

The rule also waived certain foreclosure protections for loans that met the qualified mortgage standard. Servicers could begin foreclosure proceedings sooner, which accelerated the fee cycle. Borrower advocates warned that the combination of early foreclosure and fee charging would harm vulnerable homeowners. The CFPB's own economic analysis estimated that the rule would reduce foreclosure rates, but it did not model the impact of servicing fees on borrower equity.

Since 2014, the servicing industry has consolidated. The three largest nonbank servicers—Rocket Mortgage, Mr. Cooper, and Freedom Mortgage—now handle roughly 30 percent of all mortgages, up from about 15 percent a decade ago. These firms are not subject to the same capital requirements as banks, and they rely on fee income to cover operating costs. When delinquencies rise, their profits rise. The incentive to keep borrowers in delinquency, or at least not to prevent it, is baked into the business model.

The Servicer's Side of the Ledger

Not everyone sees the fee structure as predatory. Industry representatives argue that servicing is a low-margin business where fees are essential to cover the cost of managing delinquent loans. A spokesperson for the Mortgage Bankers Association noted that servicers advance funds for taxes, insurance, and foreclosure costs, and they must be reimbursed. Without late fees and force-placed insurance, servicers would have to raise interest rates for all borrowers or exit the market, reducing credit availability.

There is some merit to this argument. Servicers are required to advance principal and interest to investors even when borrowers don't pay. They also pay for property preservation, legal fees, and escrow advances. A 2024 study by the Urban Institute estimated that the cost of servicing a delinquent loan is roughly $2,500 per year, far more than the fees collected from a single missed payment. The study concluded that fees cover only a fraction of the actual cost, but advocates dispute the methodology, noting that servicers also earn interest on escrow balances and receive float income.

The regulatory burden is also real. Since 2014, servicers have had to comply with dozens of new federal and state rules, including timely loss mitigation reviews, dual-tracking prohibitions, and strict foreclosure timelines. Compliance costs have risen sharply, and smaller servicers have been driven out of the market. The remaining large servicers argue that fees are a necessary offset to these costs.

Yet the structure of fees—particularly force-placed insurance markups and reinstatement fees—suggests that profit, not cost recovery, is the primary motive. A force-placed policy that costs the servicer $200 per month but is charged to the borrower at $500 per month generates a 150 percent margin. Such margins are hard to justify as mere cost recovery. The trade-off between fair compensation and profiteering is at the heart of the debate.

The Federal Reserve's Blind Spot

The Federal Reserve's June 2026 meeting minutes revealed a split among policymakers over the direction of interest rates. Some officials worried that higher rates could slow the economy; others feared inflation would persist. But the minutes made no mention of mortgage servicing fees or their impact on borrower distress. This blind spot matters because the Fed's rate decisions directly affect delinquency risk. When rates rise, adjustable-rate mortgages reset higher, and more borrowers miss payments. Those borrowers then face the fee machine described above.

The Fed's models of mortgage default focus on interest rates, unemployment, and home prices. They do not account for the effect of servicing fees on default probability. A borrower who owes $2,000 in late fees and force-placed insurance may be more likely to default than one who owes only the missed payment. The fees increase the total debt burden, making it harder to catch up. Yet the Fed's macroeconomic forecasts treat servicing fees as a minor friction, not a systemic risk.

Some economists have called for the Fed to include servicing fee data in its stress tests for large banks and nonbank servicers. The Financial Stability Oversight Council could designate nonbank servicers as systemically important, subjecting them to stricter oversight. So far, neither has happened. The servicing industry argues that fees are a necessary part of the business and that regulation would reduce credit availability.

The disconnect between monetary policy and servicing rules means that borrowers are exposed to risks that policymakers do not fully measure. When the Fed raises rates to cool inflation, it may inadvertently increase the fee burden on struggling homeowners. The costs are concentrated among the most vulnerable borrowers—those with low credit scores, small equity cushions, and limited access to refinancing.

What a Borrower Can Do—and What They Can't

Borrowers who miss a payment should request an escrow analysis from their servicer to ensure that force-placed insurance has not been added unnecessarily. If the borrower already has insurance, providing proof can stop the force-placed policy and trigger a refund of premiums. The servicer is required under RESPA to respond to written requests within 30 days, but enforcement is complaint-driven.

Asking for a written reinstatement breakdown is another step. The servicer must itemize all fees and charges. If a fee seems excessive, the borrower can dispute it in writing. Some state laws, like California's anti-predatory lending rules, cap late fees at 4 percent and prohibit certain processing fees. Borrowers in those states may have stronger protections.

Free housing counselors, funded by the Department of Housing and Urban Development, can help negotiate with servicers. But these counselors are underfunded and often have caseloads of hundreds of clients. A 2024 report by the National Housing Conference found that counselors spent an average of 12 hours per client, and many borrowers waited weeks for an appointment. The system works for some, but not for most.

Borrowers also have legal recourse under RESPA Section 6, which provides a private right of action for servicing violations. If a servicer fails to respond to a qualified written request or charges unauthorized fees, the borrower can sue for actual damages, statutory damages, and attorney's fees. However, litigation is expensive and time-consuming, and many borrowers cannot afford to pursue it. Class-action suits can aggregate small claims, but they require a lead plaintiff and may take years to resolve.

The Unlikely Reformers: State Attorneys General and Class-Action Firms

State attorneys general have become the de facto enforcers of servicing rules. The New York AG's 2023 settlement with Ocwen required the servicer to pay $150 million in restitution and reform its fee practices. California's Department of Financial Protection and Innovation has pursued actions against servicers for unfair fee collection. These state-level efforts have returned some money to borrowers, but they are piecemeal and slow.

Class-action law firms have used the Racketeer Influenced and Corrupt Organizations Act (RICO) to challenge fee harvesting as a pattern of fraud. In 2025, a federal judge in Florida allowed a RICO suit to proceed against a major servicer, citing allegations that the servicer charged fees for services it never performed. The case is ongoing. If successful, it could open the door to treble damages and reshape the industry. The outcome remains uncertain, but the case signals that courts are willing to scrutinize fee practices more deeply.

Federal preemption blocks many state reforms. The Dodd-Frank Act preserved state authority over servicing, but courts have sometimes ruled that federal law preempts state fee caps. A bipartisan bill introduced in 2023 would have established federal limits on late fees and force-placed insurance premiums, but it stalled in committee. Industry opposition was strong, and the bill never reached a vote.

The most promising reform may be regulatory: the CFPB could update its 2014 rule to cap servicing fees or require that fees be tied to actual costs. The agency has signaled interest in such changes, but action has been slow. The servicing industry has deep pockets and a powerful lobbying presence in Washington. Reform is possible, but it will require sustained pressure from consumer advocates, state officials, and the borrowers themselves. Until then, the fee machine grinds on, one missed payment at a time.

This article is for informational purposes only and does not constitute legal or financial advice. Borrowers facing delinquency should consult a housing counselor or attorney.