Bank Savings Withdrawal Limit That Triggered a Sixty Dollar Fee on Five Dollars

It started with a simple five-dollar withdrawal from a savings account. The account holder needed cash for a small purchase, so they transferred the money to checking. A month later, a statement arrived showing a sixty-dollar fee labeled "excess transaction." The bank had counted six withdrawals that month, and the sixth one—the five-dollar transfer—violated a monthly limit buried in the account agreement. The fee was twelve times the amount withdrawn. This is not an isolated story. It is a predictable outcome of how savings accounts are designed, regulated, and marketed.

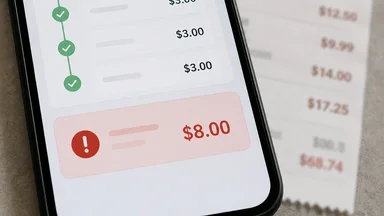

The $5 Withdrawal That Cost $60

The fee structure for excess withdrawals is straightforward on paper. Many savings accounts impose a limit on the number of certain types of withdrawals or transfers per month. Historically, this limit was six, a figure rooted in a Federal Reserve regulation known as Regulation D. Although the Fed suspended the six-per-month rule in 2020, many banks kept the limit in their own terms, and they kept the penalty fees. The fee for exceeding that limit typically ranges from five to fifteen dollars per violation, but some banks charge more. In this case, the account had a five-dollar-per-violation fee, but the bank applied it retroactively to all six withdrawals, not just the sixth one. That meant thirty dollars in fees, plus a second tier of penalties for going over the limit multiple times, bringing the total to sixty dollars.

The account holder had no idea the limit existed. The bank's online interface did not display a warning before the transfer. The monthly statement listed the fee in a dense table of charges, but by then the damage was done. The customer called the bank and asked for a waiver. The representative explained that the fee was disclosed in the account agreement, which the customer had signed electronically when opening the account. The waiver was denied. The customer then asked to close the account. The representative said the account could be closed, but the fee would still be deducted from the balance, leaving a negative balance that would be sent to collections if unpaid.

This scenario plays out thousands of times a day across the country. The Consumer Federation of America estimates that banks collect roughly $15 billion annually in overdraft and excess withdrawal fees combined. The fees are especially punishing for low-balance accounts, where a single fee can wipe out months of interest earned. The five-dollar withdrawal that cost sixty dollars is an extreme example, but it illustrates the asymmetry at the heart of the product: the bank profits from the customer's mistake, and the customer bears the full cost of a rule they likely never knew existed.

How Savings Accounts Are Designed to Trap You

Savings accounts are not just storage bins for cash. They are products with specific regulatory histories and profit incentives. The six-per-month limit originated from Regulation D, which classified savings accounts as "transaction accounts" if they allowed more than six preauthorized or automatic transfers per month. The rule was meant to distinguish savings from checking accounts for reserve requirement purposes. Banks, in turn, built their systems around this limit, and when the Fed lifted the rule in 2020, most banks chose to keep the limit anyway. Why? Because penalty fees are lucrative.

According to a 2022 Consumer Financial Protection Bureau report on bank fee revenue, penalty fees from savings account excess transactions generate significant revenue for large banks, with the largest institutions reporting over $2 billion annually in combined overdraft and excess transaction fees. The fees are often small per incident—five to fifteen dollars—but they add up across millions of accounts. Moreover, the fees are sticky: customers rarely switch banks over a single fee, and the complexity of the rule means many customers will violate it repeatedly before they learn to avoid it. Banks also benefit from consumer inertia. Once a customer has direct deposit, automatic bill pay, and a checking account linked to the savings account, the hassle of switching banks outweighs the annoyance of an occasional fee.

The design of online banking interfaces reinforces this trap. Most banks do not display a running count of withdrawals for the month. The customer sees a balance and a transfer button, but not a warning that they are approaching a limit. Some banks send an email or push notification after the fact, but by then the fee has already posted. The assumption is that the customer will read the account agreement, but the agreement is typically a dense legal document dozens of pages long. The fee schedule is buried in a section titled "Transaction Limitations" or "Excess Activity Fee." The language is precise but opaque: "If you exceed the monthly limit of six withdrawals or transfers, we may charge a fee of $10 per item." That sentence is easy to miss.

The trap is not malicious in the sense of a deliberate scam, but it is a structural feature of the product. The bank designs the account to encourage saving—hence the higher interest rate compared to checking—but also to discourage frequent withdrawals. The penalty fee is the enforcement mechanism. The customer, meanwhile, expects a savings account to be accessible for occasional needs. The mismatch between expectation and contract is where the fee lives.

The Fine Print Nobody Reads

Account agreements for savings accounts are long, but the relevant section is usually short. A typical clause reads: "You may make no more than six withdrawals or transfers from your savings account per monthly statement cycle. The following transactions count toward this limit: preauthorized transfers, automatic transfers, telephone transfers, online transfers, and overdraft transfers. If you exceed this limit, we may charge a fee of $10 per transaction." That is the entire rule. But the rule is surrounded by dozens of other clauses about interest calculation, minimum balance requirements, dormant account fees, and escheatment laws. The customer skims it, clicks "I agree," and moves on.

The problem is not that the fee is hidden. It is that the fee is disclosed in a format that is not designed to be read. The disclosure is legally sufficient, but practically useless. The bank knows this. The bank also knows that most customers will not call to ask about the limit before making a withdrawal. The bank relies on the fact that the customer will discover the fee only after it has been charged, and that the customer will be less likely to switch banks than to accept the fee and move on.

Some banks have tried to soften the blow by offering one fee waiver per year. Others automatically waive the fee if the account balance is below a certain threshold. But these policies are not standardized, and they are not advertised. The customer who calls to ask for a waiver may get it, but only if they ask. The customer who does not call pays the fee. The asymmetry is baked into the system.

There is also the issue of how the limit is calculated. Some banks count each withdrawal separately, even if multiple withdrawals are made on the same day. Others count only certain types of transfers—online transfers count, but in-person withdrawals at a teller do not. Still others have a combined limit for all electronic transfers, regardless of destination. The variation across banks is wide, and the customer has no way of knowing the specific rules without reading the fine print. The fine print is the only source of truth, and it is written in a language that is not designed for easy comprehension.

Comparing Fee Structures Across Big Banks

The excess withdrawal fee varies by institution, but the pattern is consistent. Chase charges $10 per transaction after the limit is exceeded. Bank of America assesses $12 per item. Wells Fargo imposes $15 per violation. Credit unions tend to be cheaper, with fees in the $5 to $10 range. Some online banks, like Ally and Capital One 360, have eliminated the limit entirely or reduced the fee to zero. But the big brick-and-mortar banks have largely kept the fee in place.

The limit itself also varies. Most banks set the cap at six transactions per month, but some have lowered it to three. Others have a tiered structure: six transactions are allowed, but after that, each transaction incurs a fee. A few banks have a hard limit: after six withdrawals, the account is converted to a checking account or restricted from further withdrawals until the next cycle. The conversion can trigger additional fees, such as a monthly service fee for the checking account.

For a customer with a low balance, the math is brutal. If the account earns 0.01% interest, a $500 balance earns about five cents per year. A single $10 fee wipes out 200 years of interest. The fee is not a deterrent to overuse; it is a penalty that far exceeds any benefit the customer receives from the account. The bank, meanwhile, earns the fee as pure profit, minus the cost of processing the transaction.

The fee structure also interacts with overdraft protection. Many customers link their checking account to their savings account for overdraft coverage. If the checking account is overdrawn, the bank automatically transfers funds from savings to cover the shortfall. That transfer counts as a withdrawal from savings. If the customer has already made six withdrawals that month, the overdraft transfer triggers an excess fee. The customer then pays a fee for the overdraft protection that was supposed to save them money. It is a double hit.

Why Banks Keep the Limits: A Counter-Argument

It is easy to cast banks as villains, but the withdrawal limit is not arbitrary. Banks have legitimate operational and regulatory reasons for maintaining the six-per-month cap. First, savings accounts are classified differently from checking accounts under banking regulations. Even after the Fed suspended Regulation D, savings accounts still carry reserve requirements that differ from checking accounts. If every savings account behaved like a checking account, banks would need to hold more reserves, which could reduce the interest rates they offer on savings. Second, frequent withdrawals increase administrative costs for the bank—each transfer requires processing, reconciliation, and fraud monitoring. The limit helps keep those costs predictable. Third, the limit encourages the behavior that savings accounts are designed for: saving. A customer who treats a savings account like a checking account is more likely to spend the money, which defeats the purpose of the account.

Some customers actually benefit from the limit. For example, a customer who struggles with impulse spending may appreciate the friction that a withdrawal limit creates. The limit acts as a speed bump, making it harder to drain savings on a whim. For these customers, the fee is a deterrent that reinforces good habits. Additionally, banks that offer higher interest rates on savings accounts often rely on the limit to keep their cost of funds low. Without the limit, those rates might be lower. The trade-off is real: the customer who wants unlimited withdrawals may have to accept a lower interest rate or pay a monthly fee.

The key is that the limit is not inherently predatory. It becomes a problem when it is poorly disclosed, when the fee is disproportionately high relative to the transaction, and when the customer is not given tools to track their usage. The criticism should focus on transparency and fee proportionality, not on the existence of the limit itself.

When the Fee Becomes a Trap for Low Balances

Small savers are the most vulnerable to these fees. A customer with a $100 savings balance who makes a $20 withdrawal and triggers a $10 fee has lost 10% of their balance in a single transaction. If the fee is applied to multiple transactions, the balance can go negative quickly. A negative balance can then trigger an account closure, and the bank may report the unpaid fee to a credit bureau. The customer's credit score takes a hit over a fee that was, in many cases, avoidable only if the customer had known the rule.

Banks have faced regulatory scrutiny over these practices. The Consumer Financial Protection Bureau has issued guidance on overdraft fees and has taken enforcement actions against banks that engaged in deceptive practices. But the excess withdrawal fee has largely escaped the spotlight. It is not an overdraft fee, so it is not subject to the same rules. It is a fee for exceeding a contractual limit, and as long as the limit is disclosed, the fee is legal. The burden is on the customer to read the contract and track their withdrawals.

The trap is especially pernicious for customers who use their savings account as a de facto checking account. Some customers keep their main balance in savings to earn higher interest and transfer money to checking as needed. If they make more than six transfers in a month, they incur fees that erase any interest benefit. The customer who thinks they are being smart by maximizing interest is actually being penalized for behavior that the bank's own marketing encourages.

How to Avoid the Fee Without Closing the Account

The simplest way to avoid the fee is to track the number of withdrawals manually. A customer can keep a running tally on a notepad or in a spreadsheet. Some banks offer alerts that can be set to notify the customer when they have made a certain number of withdrawals. But the alerts are not always reliable, and they are often set to trigger after the fact. A better approach is to limit savings account withdrawals to emergencies and to use a checking account for all routine transactions.

Another strategy is to link the savings account to overdraft protection but to keep a buffer in checking. If the checking account has enough funds to cover most purchases, the overdraft transfer is rarely triggered. The customer can also set up automatic transfers from checking to savings on a regular schedule, which counts as a withdrawal from checking, not savings. The key is to minimize the number of times money moves out of the savings account.

For customers who need frequent access to their savings, a money market account may be a better fit. Money market accounts often allow check writing and debit card access, and they may have higher withdrawal limits or no limits at all. The trade-off is that money market accounts typically require a higher minimum balance and may have lower interest rates than high-yield savings accounts. But for a customer who needs liquidity, the flexibility is worth the lower rate.

Some online banks and credit unions offer savings accounts with no withdrawal limits and no excess fees. These accounts are often called "high-yield savings accounts" or "no-penalty savings accounts." They may have lower interest rates than accounts with limits, but the absence of fees means the customer can use the account freely. The customer should read the terms carefully, because some accounts that claim to have no limits still impose a fee after a certain number of transactions, just at a higher threshold.

Finally, the customer can simply close the savings account and move the money to a checking account that pays interest. High-yield checking accounts are now widely available, and some offer interest rates comparable to savings accounts. The checking account may have no withdrawal limits, and the customer can use it for all transactions without worrying about fees. The downside is that checking accounts often have monthly service fees that can be waived with direct deposit or a minimum balance. The customer needs to compare the total cost of the checking account against the potential fees of the savings account.

The Better Alternative: No-Limit Savings or High-Yield Checking

The banking industry has slowly moved toward products that eliminate the withdrawal limit. Online banks like Ally, Marcus by Goldman Sachs, and Discover have savings accounts that do not charge excess fees, even if they technically have a limit. These banks have automated systems that warn the customer before a withdrawal would exceed the limit, and they rarely enforce the fee. The reason is competitive pressure: online banks compete on customer experience, and a fee that punishes customers for using their own money is a bad experience.

Credit unions have also been more flexible. Many credit unions offer share savings accounts with no monthly limit on withdrawals, or they cap the fee at a low amount. Credit unions are member-owned, so the incentive to maximize fee income is weaker. A customer who belongs to a credit union can often make unlimited withdrawals from savings without penalty. The trade-off is that credit unions may have lower interest rates and fewer branches, but for many customers, the flexibility is worth it.

High-yield checking accounts are another alternative. These accounts pay interest on the balance, often with tiered rates that increase with the balance or with the number of debit card transactions. The interest rate may be lower than the best savings accounts, but the account has no withdrawal limits. The customer can use the account for all transactions, including bill pay, debit card purchases, and ATM withdrawals. The key is to find a checking account that does not charge monthly maintenance fees and that offers free ATM access.

The decision between a savings account and a checking account depends on the customer's cash flow patterns. A customer who saves a large portion of their income and rarely touches the savings may benefit from a high-yield savings account with a limit, because the interest rate is higher and the fees are avoidable. A customer who needs frequent access to their savings—for irregular expenses, for example—should choose an account with no limit or a checking account that pays interest. The customer should also consider the bank's customer service reputation, because a bank that is willing to waive fees on request is better than one that enforces every letter of the contract.

The fee structures described here are not static. Banks periodically revise their terms, and regulatory changes could alter the landscape. For now, the best defense is knowledge: read the account agreement, track your withdrawals, and choose an account that aligns with your actual usage. If you do incur a fee, call the bank and ask for a waiver—many banks will grant one, especially for first-time offenders. And if the bank refuses, consider moving your money to an institution that offers more transparent terms. The market is competitive enough that you have options.

This article is for informational and educational purposes only. It does not constitute personalized financial advice or a recommendation for any specific financial product or service. Readers should review their own account agreements, consider their individual financial circumstances, and consult with a qualified professional before making changes to their banking arrangements.