Checking Account Fee That Charges You for the Same Money Twice in One Day

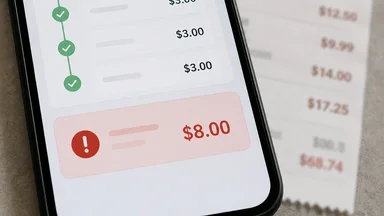

Imagine depositing a $100 check into your checking account, only to have your bank charge you two separate fees—each roughly $34—for the same transaction, on the same day. This isn't a glitch. It's a fee structure that some of the largest U.S. banks use, and it can turn a routine deposit into a $68 hit. The practice is known as the same-dollar double dip, and it affects millions of account holders whose balances hover near zero.

The double fee scenario usually unfolds like this: You write a check or authorize a debit for, say, $100, but your account balance is only $50. The bank processes the transaction and charges an insufficient-funds penalty—typically in the range of $30 to $40—because the check bounces. But the bank also pays the $100 on your behalf, pushing your balance to negative $50. Then, because your account is now negative, the bank hits you with a second fee: an overdraft charge, also around $30 to $40. You now owe $50 plus $60 to $80 in fees, all on a single $100 transaction.

Consumer complaints filed with the Consumer Financial Protection Bureau (CFPB) routinely describe this exact pattern. A 2025 CFPB report noted that some banks charge both a returned-item fee and an overdraft fee on the same transaction, and that these fees can total more than $70 per incident. For a low-balance account holder, that can mean losing 10% or more of their monthly income to a single fee cycle.

The key to understanding the double dip is knowing that banks often process transactions in a specific order—largest to smallest—which maximizes the number of fees. If a $100 check arrives after a $50 debit, the bank may post the $100 first, triggering an overdraft on the $50 debit, then charge a second fee on the $100. The same dollars are used to calculate two fees, but the bank treats them as separate events.

Why a Single Transaction Can Trigger Both a Returned-Item Fee and an Overdraft Fee

The return-item fee is charged when a check or electronic payment is presented for payment but the account lacks sufficient funds. The bank returns the item unpaid and charges a fee for the processing. The overdraft fee, on the other hand, is charged when the bank covers a transaction that exceeds the available balance, effectively lending you the money. If the bank both returns the item and then covers it—or if the sequence of postings makes it appear that two separate transactions occurred—both fees can apply.

The sequencing of postings is a critical factor. Banks typically process transactions in high-to-low dollar order, a practice that has been criticized by regulators. Under this order, a large check might be posted first, depleting the balance, and then a smaller debit posted later triggers a second overdraft. Even if the large check later bounces, the bank may still keep the overdraft fee on the second transaction. This practice can turn a single day's activity into a cascade of fees.

The CFPB has scrutinized this practice. In 2025, the agency proposed a rule that would cap overdraft fees at roughly $3 per transaction, but the rule has faced legal challenges from the banking industry. As of mid-2026, the rule has not been implemented, and banks continue to charge fees that can exceed $40 each. Some banks have voluntarily simplified their fee structures, but many still rely on the double-charge model for revenue.

Consumer advocates argue that the double fee is inherently unfair because it charges a customer twice for the same shortfall. Industry representatives counter that each fee covers a distinct service: one for the administrative cost of returning the item, and another for the risk of advancing funds. The debate hinges on whether those costs are truly separate, or whether the bank is simply double-counting the same risk.

The Biggest Banks That Use This Double-Charge Model

JPMorgan Chase, Wells Fargo, and Bank of America—three of the largest U.S. banks by assets—all charge overdraft and returned-item fees that can combine into a double charge. As of early 2026, each bank's standard overdraft fee is roughly $34 per occurrence, and returned-item fees are similarly priced. While some banks have introduced "grace days" or small-dollar fee waivers, the double charge remains possible for any transaction that pushes an account negative.

Chase, for example, charges an overdraft fee of $34 and a returned-item fee of $34. If a check bounces and the bank covers it, both fees can apply. Wells Fargo charges $35 for both overdraft and returned-item fees, and Bank of America charges $35 as well. These fees are among the highest in the industry. Some regional banks charge even more, with some hitting the $41 mark.

Credit unions, by contrast, often avoid this practice. Many credit unions charge lower fees—sometimes as low as $20—and some have eliminated overdraft fees entirely. The Credit Union National Association reports that the average credit union overdraft fee is about $28, and many credit unions do not charge a returned-item fee if the item is small. For consumers who want to avoid the double dip, switching to a credit union or a community bank can be a straightforward solution.

However, not all big banks are equally aggressive. Some, like Capital One, have eliminated overdraft fees altogether. Others, like U.S. Bank, offer a "low balance" alert system that can help customers avoid fees. The key is to check the fee schedule and ask whether a single transaction can trigger both fees. Bank representatives may not volunteer this information, but a direct question can reveal the policy.

How Deposit Timing and Settlement Rules Enable the Double Fee

Deposit timing plays a crucial role in whether a double fee occurs. When you deposit a check, the bank may place a hold on the funds for up to two to five business days under Regulation CC. Even if you deposit cash, the bank may not credit the funds until the next business day. If a check or debit arrives during that hold period, the bank may treat the balance as insufficient, even if the deposit is pending.

Same-day cash deposits are not immune. If you deposit cash after the bank's cut-off time—typically 5:00 p.m. local time—the funds may not post until the next day. A debit that processes overnight or early the next morning can still trigger fees. Weekend deposits are especially risky, as many banks do not process transactions on Saturdays or Sundays, leaving a longer window for pending debits to cause overdrafts.

The automated posting systems at many banks run at 12:01 a.m. each day. If a deposit is scheduled to post later that day, but a debit posts first, the system sees a negative balance and charges a fee. Some banks offer "courtesy pay" programs that allow transactions to go through even when the balance is low, but these programs often come with a fee that is charged per transaction, not per day.

The combination of hold periods, cut-off times, and automated posting means that consumers can be charged a double fee even if they have sufficient funds in the account but the deposit hasn't cleared. The CFPB has suggested that banks should provide real-time balance information and allow consumers to opt out of overdraft coverage for everyday debit transactions, but these measures are not yet universal.

Three Strategies to Never Pay the Twice-a-Day Fee Again

Opt out of overdraft coverage for debit card and ATM transactions under Regulation E. This means that if you try to make a debit card purchase without sufficient funds, the transaction will be declined, and you won't be charged a fee. You can opt out by calling your bank or updating your account settings online. This does not stop check or ACH transactions from triggering fees, but it eliminates the most common source of overdrafts.

A second strategy is to link your checking account to a savings account for automatic overdraft transfer. Many banks offer this service for a small fee—typically $10 to $12 per transfer—which is much lower than a $34 overdraft fee. Some banks, like Bank of America, allow up to two transfers per day for a flat fee. This can turn a $68 double fee into a $12 single fee. However, you need to have sufficient funds in the savings account to cover the transfer.

Third, consider using a prepaid card or a second bank account as a buffer. Prepaid cards typically do not allow overdrafts, so you cannot be charged a fee. Some online banks, like Chime and Ally, offer fee-free overdraft protection up to a small limit. A second checking account at a different bank can serve as a backup: if your primary account is low, you can transfer funds from the second account before a transaction hits. This requires discipline, but it can save hundreds of dollars a year.

Finally, if you do get hit with a double fee, you can ask the bank for a one-time courtesy waiver. Many banks will waive the first fee if you call and explain the situation. Some banks, like Wells Fargo, have a policy of waiving one overdraft fee per year for customers who ask. It's not a guarantee, but it's worth a five-minute phone call.

What Regulators Have Done So Far—and What They Haven't

The CFPB has been the most active regulator on overdraft fees. In January 2025, the agency proposed a rule that would limit overdraft fees to roughly $3 per transaction for large banks, a dramatic reduction from the current $30–$41 range. The rule also would require banks to treat overdraft services as credit products, subject to Truth in Lending Act disclosures. The banking industry sued to block the rule, and as of mid-2026, the rule has not taken effect.

The CFPB's 2025 proposal was based on data showing that banks collect roughly $9 billion annually in overdraft and NSF fees, with the bulk coming from a small number of frequent users. The agency argued that the actual cost to banks of processing an overdraft is less than $1, making the current fees excessive. Banks countered that the fees cover not only processing costs but also the risk of non-repayment and the cost of maintaining the overdraft infrastructure.

Other regulators have been less aggressive. The Office of the Comptroller of the Currency (OCC) and the Federal Reserve have issued guidance encouraging banks to reduce reliance on overdraft fees, but they have not imposed a cap. Some states have taken action: for example, California and New York have considered legislation to limit overdraft fees, but no federal ban on double-dipping exists.

The current situation is a mix of voluntary reforms and legal uncertainty. Some banks have voluntarily eliminated overdraft fees—Ally Bank, Capital One, and Citibank are notable examples. Others have reduced fees or introduced grace periods. But the majority of large banks still charge the double fee, and the CFPB rule remains tied up in court. For now, the burden is on the consumer to understand their bank's fee schedule and take steps to avoid the double dip.

The True Cost of the Double Fee Over a Year

For a consumer who experiences the double fee six times per year—a conservative estimate for someone living paycheck to paycheck—the annual cost can range from roughly $200 to $480, depending on the bank's fee amounts. At $34 per fee, six double-dip incidents (each with two fees) cost $408. At $41 per fee, the cost is $492. These are not trivial amounts for households with limited savings.

The compound effect is even worse. When fees push an account negative, the consumer may incur additional fees from merchants (for returned checks) or from the bank for subsequent transactions that fail. A single double-fee incident can spiral into a cascade of fees, easily exceeding $100. The CFPB has noted that frequent overdraft users pay an average of $450 per year in fees, with some paying over $1,000.

Alternative accounts—such as those at credit unions or online banks—often charge no overdraft fees or much lower fees. For example, a credit union that charges $20 per overdraft and does not charge a returned-item fee could reduce the annual cost to $120 for the same six incidents. That's a savings of $288 compared to a bank charging $34 per fee. Even after accounting for potential inconvenience, the savings can be substantial.

However, switching banks is not always easy. Some consumers have direct deposit or automatic bill payments set up with their current bank, and changing those can take time. Others may have a negative balance that prevents them from closing the account. For these consumers, the best approach is to use the strategies outlined above—opt out of overdraft, link a savings account, or use a prepaid card—to minimize fees while they plan a transition.

The double fee is not a law of banking; it is a choice banks make. By understanding how it works and taking proactive steps, consumers can avoid paying for the same money twice. The fee exists because bank fee structures are not always aligned with customer interests. Until regulators act more decisively, the burden remains on the consumer to navigate a system that can charge $68 for a $100 mistake.

Disclaimer: This article is for informational purposes only and does not constitute personalized financial advice. Consult a qualified professional for advice tailored to your specific situation.