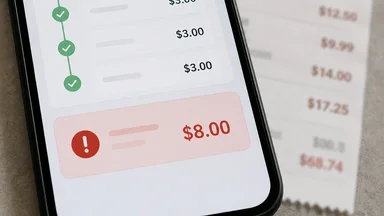

Buy Now Pay Later Late Fee That Exceeds the Original Purchase Amount in Days

You tap your phone to buy a $12 sandwich combo using a Buy Now Pay Later (BNPL) app. Four installments of $3 each, no interest. You miss a payment — maybe the autopay card expired, maybe you just forgot. The late fee is $8 per missed installment. After four missed payments, you owe $32 in fees on a $12 sandwich. That is not a penalty; it is a loan at an effective annual percentage rate that would make a payday lender blush. This is not a hypothetical edge case. The Consumer Financial Protection Bureau flagged this exact dynamic in its 2025 market report, and the numbers have only grown since.

BNPL contracts typically allow late fees of up to $8 per missed installment, though the exact cap varies by provider and state. For a four-payment plan, missing all four installments can generate $32 in fees on a $12 purchase. That is a 267% fee relative to the original amount. Even if you catch up after one missed payment, the $8 fee represents 67% of the $12 item. State-level fee caps often limit late fees to a percentage of the purchase — typically 20–30% — but those caps apply per installment, not per order, and some states exempt BNPL from usury laws entirely. For example, in California, the Department of Financial Protection and Innovation has noted that late fees are not interest, so they fall outside the state's usury cap. This loophole means that a $7 late fee on a $5 coffee is perfectly legal, even though the effective rate is astronomical.

The CFPB's 2025 report noted that roughly 10–15% of BNPL users incur at least one late fee in a given year. For low-dollar purchases, the fee-to-purchase ratio can be extreme. A $5 coffee paid in four installments of $1.25, with a $7 late fee per missed payment, means a single slip-up costs more than the coffee itself. The industry argues that such cases are rare and that most users pay on time. But rare does not mean nonexistent, and the contract allows it. Moreover, the frequency of late fees is not evenly distributed: a 2024 study by the Consumer Federation of America found that frequent BNPL users — those who take out more than ten plans per year — incur late fees at nearly double the rate of occasional users, suggesting that the product's design encourages repeat borrowing and increases the likelihood of missed payments.

Providers like Afterpay and Klarna disclose these fees in their terms of service, but the disclosures are often buried. Afterpay's standard late fee is $8 per order in some states, capped at 25% of the order value for larger purchases. For small purchases, the cap is effectively meaningless because the flat fee exceeds the percentage cap. The CFPB's 2025 interpretive rule proposal attempted to classify BNPL as a credit card product, which would trigger Truth in Lending Act disclosures, but the rule has not been finalized. As of mid-2026, the rule remains in limbo, with industry lobbying efforts focused on preserving the current disclosure regime. The trade-off here is between consumer protection and innovation: stricter rules might reduce fee abuse but could also limit access to short-term credit for consumers who cannot qualify for traditional cards.

The $30 Late Fee on a $12 Purchase

Consider a concrete example. A consumer in Texas buys a $20 fast-casual meal using a four-installment BNPL plan from Provider X. The first installment of $5 is due at checkout. The remaining three installments are due every two weeks. The consumer sets up autopay but later switches bank accounts and forgets to update the payment method. The second installment is missed. Provider X charges a late fee of $7 per missed installment, with a grace period of 10 days. The consumer pays the $5 installment plus the $7 fee after 12 days, but the fee is already applied. Meanwhile, the third installment is due in four days. If the consumer misses that as well, another $7 fee applies. Total fees for two missed installments: $14 on a $20 purchase — 70% of the original price. The consumer might never see the fee structure until it appears on their next statement, because the app only shows the installment amount and the next due date, not the cumulative fee risk.

State-level fee caps vary widely. In New York, late fees on credit products are generally capped at $30 per occurrence, but BNPL providers have argued that their products are not credit under state law because they do not charge interest. This argument has held in some courts, leaving consumers without the protections that apply to traditional credit cards. In contrast, the European Union's Consumer Credit Directive, updated in 2023, caps late fees at the cost of the credit plus a reasonable penalty, effectively preventing the kind of fee cascades seen in the US. The US regulatory patchwork means that a consumer in one state might face fees that are illegal in another, creating confusion and unequal protection.

The CFPB's 2025 report also highlighted that late fees disproportionately affect low-income consumers. BNPL users are more likely to have subprime credit scores and lower incomes than traditional credit card users, according to the report. For these consumers, a $8 late fee can be a significant financial shock, especially when combined with other fees from overdrafts or returned payments. The report estimated that BNPL users are roughly 40% more likely to incur bank overdraft fees than non-users, suggesting that the payment method itself introduces risk. The industry response has been to emphasize financial literacy and reminder systems, but critics argue that the product's design exploits behavioral biases rather than educating consumers.

How the Fine Print Turns a Fee Into a Loan

The late fee on a BNPL plan is not a simple penalty; it is deferred interest disguised as a service charge. Most BNPL agreements waive the fee if you pay within a grace period — typically 7 to 10 days after the due date. But that grace period is buried in the terms of service, often in a section titled "Late Payment Policy" or "Default Charges." If you miss the grace window, the fee is applied retroactively to the missed installment, and interest does not accrue because the product is structured as a zero-APR loan. Instead, the fee is a flat charge that can be applied repeatedly. This structure creates a perverse incentive for providers: they profit not from interest but from fees, which are less regulated and less visible to consumers.

Consider how this works in practice. You buy a $40 sweater with a four-installment BNPL plan. The first installment of $10 is due at checkout. The remaining three are due every two weeks. You miss the second installment by one day. The provider charges an $8 late fee. You pay the $10 plus $8, but the late fee is added to your balance. The third installment is now $10 plus any additional fees if you miss again. Some providers, like Affirm, cap late fees at 25% of the purchase price, but that cap is per installment, not per order. On a $40 purchase, the cap is $10 per installment, so three missed installments could generate $30 in fees — 75% of the original price. In contrast, Afterpay charges a flat $8 per order in many states, which means that even if you miss multiple installments, you only pay one $8 fee. This difference is not obvious from the marketing materials, which all emphasize "no interest" and "four easy payments."

The fine print also determines whether the fee is per installment or per order. Afterpay charges a late fee per order, not per installment, which is more consumer-friendly. But Klarna and other providers may charge per missed installment, creating a cascade. The difference is buried in the contract's definitions section. The CFPB's 2025 market report found that consumers who read the terms were still confused about when fees applied, suggesting that disclosure alone is insufficient. Behavioral research supports this: even when consumers are presented with clear fee information, they tend to underestimate the probability of missing a payment, and they discount future fees relative to the immediate benefit of the purchase. This is the same psychological mechanism that makes payday lending profitable: people focus on the upfront cost and ignore the tail risk.

The Hidden Economics of Fee Cascades

One missed payment can trigger late fees on all remaining installments, even if you catch up immediately. This is the fee cascade. You miss the second installment on a four-payment plan. The provider charges an $8 late fee on that installment. But the contract may also treat the missed payment as a default on the entire order, accelerating the remaining installments and applying late fees to each. Some providers waive this if you pay the missed installment within a few days, but not all do. For example, Klarna's terms state that if a payment is more than 7 days late, the full outstanding balance becomes due immediately, and late fees may apply to each installment. This means that a single slip-up can trigger a cascade of fees that far exceeds the original purchase.

Fee revenue accounts for roughly 10–15% of BNPL income, according to industry estimates cited by the CFPB. That is not trivial. For a company like Klarna, which processed over $50 billion in transactions in 2025, fee revenue could be in the hundreds of millions. The providers argue that fees are transparent and that they offer multiple reminders before charging. Klarna, for example, sends email and push notifications before a due date and again after a missed payment. But the reminders do not change the contract terms. Moreover, the reminders themselves can be ineffective if the consumer has changed phone numbers or email addresses, or if the notifications are filtered as spam. A 2024 study by the Pew Charitable Trusts found that one-third of BNPL users reported receiving no reminder before a late fee was applied, despite provider claims to the contrary.

Beyond the fees themselves, some BNPL providers report missed payments to credit bureaus. Affirm reports to Experian and TransUnion for some products; Klarna and Afterpay do not report positive payment history but may report delinquencies. A missed payment can ding your credit score, making it harder to get a mortgage or car loan. The CFPB's 2025 report highlighted this as a growing concern, especially for younger consumers who use BNPL as their first credit product. The reporting is not uniform, and consumers may not know which provider reports until they check their credit report. For example, a consumer who misses a $10 installment on an Affirm loan might see their credit score drop by 50 points, even though the purchase was small. This creates a disproportionate penalty: a small mistake can have long-term consequences that far exceed the original purchase amount.

Why Regulators Are Circling But Not Acting

The regulatory landscape for BNPL late fees is a patchwork. The CFPB proposed an interpretive rule in 2024 that would treat BNPL like credit cards under the Truth in Lending Act, requiring standardized disclosures and dispute rights. That rule has not been finalized, and industry lobbying has been intense. The Federal Reserve Board, in June 2026, requested comment on a proposal requiring payment stablecoin issuers to maintain customer identification programs, but that rule does not directly address BNPL late fees. State-level interest rate caps do not cover late fees because the fees are classified as penalties, not interest. This classification is a key regulatory gap: penalties are subject to less scrutiny than interest rates, even though the economic effect is the same.

The industry's primary argument is self-regulation. The Financial Technology Association, which counts Affirm, Klarna, and Afterpay as members, has published best practices that include capping late fees at 25% of the purchase price and providing grace periods. But these are voluntary, and enforcement is left to the companies. The CFPB's 2025 report found that compliance with even these voluntary standards was uneven. Some providers cap fees at 25% but apply the cap per installment; others apply it per order, which is more restrictive. The report also found that some providers charged late fees even when the consumer had a pending dispute, which would be prohibited under credit card rules. The industry argues that extending credit card rules to BNPL would be burdensome because BNPL transactions are small and short-term, but consumer advocates counter that the same rules should apply to any form of credit that can generate fees exceeding the purchase amount.

State attorneys general have started to take notice. California's Department of Financial Protection and Innovation has issued guidance reminding BNPL providers that they must comply with the state's lending laws, but enforcement actions remain rare. In 2025, the New York Attorney General's office launched an investigation into BNPL fee practices, but no public action has been taken as of mid-2026. The industry argues that regulation would increase costs and reduce access to credit for consumers who cannot get traditional credit cards. That is a legitimate trade-off. But the trade-off is between access to credit and protection from fee cascades that can exceed the purchase amount. The question is whether the current level of access justifies the current level of risk, especially for vulnerable consumers.

The Psychology of 'Free' Credit

The zero-interest framing of BNPL makes it easy to ignore late fees. Behavioral studies on consumer credit show that people mentally discount small fees that are contingent on future events. The late fee is a low-probability event in the consumer's mind — until it happens. The BNPL interface reinforces this by emphasizing the installment amount and the absence of interest, while the late fee is relegated to a dropdown or a link to the terms. For example, the checkout page for a typical BNPL app shows the installment amount in large green text, with a small gray link that says "See terms." Clicking that link opens a dense page of legal language that few consumers read. This design choice is not accidental: it exploits the human tendency to focus on immediate benefits and ignore distant costs.

Autopay enrollment reduces the risk of late fees, but it does not eliminate it. If the linked card is declined or the bank account has insufficient funds, the payment fails and the late fee applies. Some providers charge a returned-payment fee on top of the late fee, adding another layer of cost. The CFPB's 2025 report noted that BNPL users are roughly 40% more likely to incur bank overdraft fees than non-users, suggesting that the payment method itself introduces risk. A consumer who uses BNPL for multiple purchases may have several autopay dates scattered across the month, increasing the chance that a single low balance triggers multiple fees. This is especially problematic for consumers with irregular income, such as gig workers or freelancers, who may not have a predictable cash flow.

The psychology also works in the provider's favor. Because the fees are small in absolute terms — $8 here, $10 there — consumers often pay them without complaint. The cumulative effect, however, can be significant. A 2024 study by the Consumer Federation of America estimated that BNPL users paid an average of $35 in late fees per year, but for frequent users, the average was over $100. That is not a trivial amount for a product marketed as free. Moreover, the fees are often hidden in the sense that they are deducted from the next payment automatically, so the consumer may not even notice the charge. This lack of friction makes it easy for providers to collect fees without consumer pushback.

Three Contract Clauses to Read Before You Tap

First, look for the late fee cap and how it is calculated. Is the cap a percentage of the purchase price or a flat dollar amount? Is it applied per installment or per order? Affirm's terms, for example, cap late fees at 25% of the purchase price, but the cap is per installment, not per order. Afterpay caps at $8 per order in many states, which is simpler. The difference matters for small purchases. For a $10 purchase, a per-installment cap of 25% means a maximum of $2.50 per missed installment, but a flat $8 fee would be 80% of the purchase price. Conversely, for a $200 purchase, the flat $8 fee is only 4%, while the per-installment cap could be higher if multiple installments are missed. Knowing which structure applies to your purchase can help you estimate the worst-case scenario.

Second, check the grace period. Most providers offer 7 to 10 days after the due date before a late fee is charged, but some have no grace period at all. The grace period may also apply only to the first missed payment, not subsequent ones. Klarna's terms, as of late 2024, include a grace period of 7 days for each installment, but the fee is applied retroactively if you miss the grace window. That means you still owe the fee even if you pay within the grace period on a later installment. Some providers also offer a one-time fee waiver if you contact customer service, but this is not guaranteed. A 2025 survey by the Consumer Reports found that only about half of consumers who requested a fee waiver received one, and the process often required a phone call and explanation.

Third, identify whether the provider reports missed payments to credit bureaus. Affirm reports to Experian and TransUnion for some products; Klarna and Afterpay do not report positive history but may report negative information. If you are building credit, a BNPL product that does not report positive payments is not helping your score, but a missed payment can hurt it. The contract may say "we may report information about your account to credit bureaus," which is vague. Look for specific language about which bureaus and under what circumstances. Some providers, like Sezzle, do not report at all, which means that late fees are the only consequence. Others, like Affirm, report both positive and negative information, so on-time payments can help your credit, but missed payments can cause significant damage. The trade-off is clear: if you want to build credit, you need to be disciplined about payments; if you are unsure, a non-reporting provider may be safer.

These clauses are not hidden, but they are dense. Reading them takes time, and the interface encourages you to skip them. But the cost of skipping can be more than the purchase itself. As regulators continue to debate the proper framework for BNPL, consumers are left to navigate a complex landscape on their own. Until rules are standardized, the best defense is to read the fine print, set reminders, and treat BNPL as a form of credit with real consequences — not as free money.

This article is for informational purposes only and does not constitute legal or financial advice. Consult a qualified professional for personalized guidance.